The S&P 500 ended the two weeks slightly lower after alternating between declines and partial rebounds. From October 3 to 10, the index declined by 2.43% from 6,715.79 to 6,552.51. The following week, from October 10 to 17, it regained some ground, rising from 6,552.51 to 6,664.01, a 1.70% increase. Overall, the market experienced a modest 0.73% decrease over the two weeks.

Nasdaq, home to tech giants like Nvidia, Apple, and Microsoft, has found itself in the spotlight for a different reason. The exchange has seen a surge in penny-stock listings from small overseas firms, many of them Chinese, with questionable financials. Facing mounting criticism that these listings invite manipulation and investor losses, Nasdaq formally requested the SEC on September 3 to tighten listing standards for such firms. The proposal, aimed at curbing risky IPOs, is still awaiting SEC approval, which could take several months.

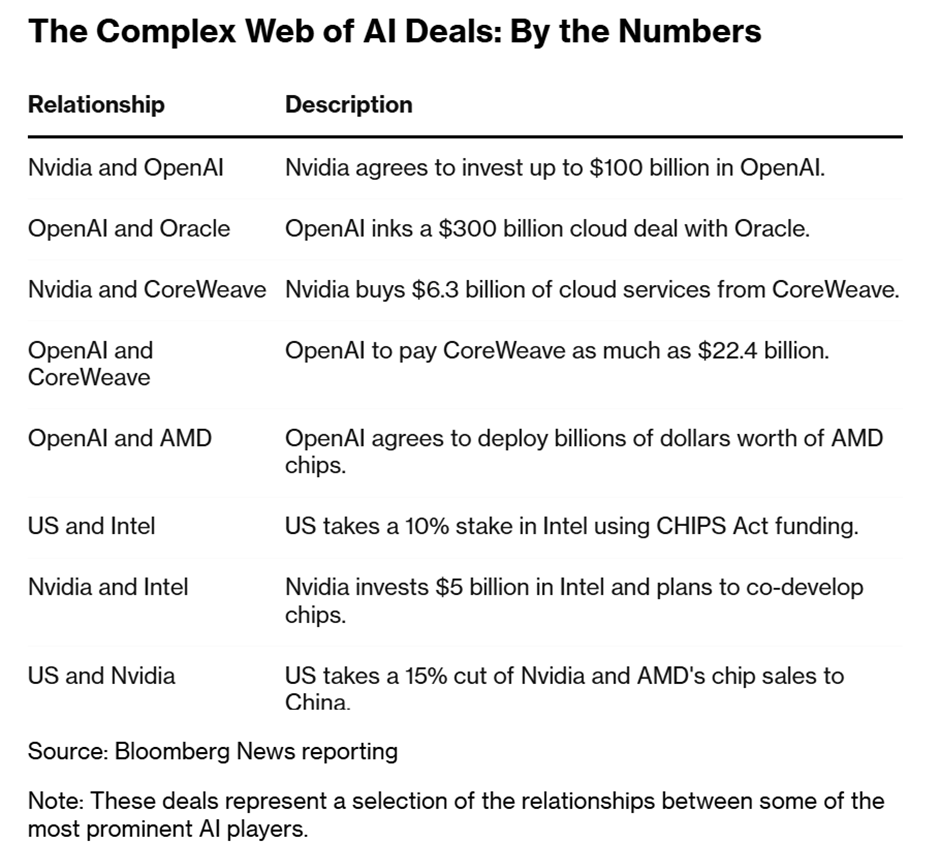

Meanwhile, concerns are rising that the trillion-dollar AI rally may be built on increasingly intertwined financial relationships. Nvidia’s agreement to invest up to $100 billion in OpenAI, announced two weeks ago, has drawn particular scrutiny. OpenAI, in turn, pledged to equip its massive new data centers with millions of Nvidia chips. Critics have labeled the deal “circular,” suggesting it keeps the AI boom alive through mutual reinforcement rather than genuine demand.

The pattern extends further: Nvidia plans to invest up to $2 billion in Elon Musk’s xAI, while also buying $6.3 billion worth of cloud services from CoreWeave, a firm in which Nvidia holds a 7% stake. CoreWeave, for its part, invested $350 million in OpenAI before its IPO and recently expanded its AI cloud contracts to $22.4 billion. Analysts warn that this web of financial interdependence could amplify market risks if AI sentiment falters. As Bernstein’s Stacy Rasgon put it, Altman “has the power to crash the global economy for a decade or take us all to the promised land.”

Beyond the AI headlines, fiscal worries in major economies are driving what investors call the “debasement trade.” Capital is flowing out of fiat currencies and into perceived safe havens like Bitcoin, gold, and silver. Gold soared past $4,300 per troy ounce last week, marking a new all-time high, fueled by inflation fears, geopolitical tension, and persistent tariff uncertainty.

The US-China trade standoff continued to escalate. Beijing’s new export limits on rare-earth minerals prompted President Trump to threaten 100% tariffs and additional export controls on “any and all critical software.” Yet, in a rare moment of restraint, Trump admitted in an interview that such tariffs “aren’t sustainable” long-term. Treasury Secretary Scott Bessent is scheduled to meet Chinese Vice Premier He Lifeng to discuss easing tensions.

At home, the Federal Reserve signaled growing caution. Chair Jerome Powell warned that the hiring slowdown poses economic risks, suggesting that more rate cuts could be on the horizon. The Fed’s September projections indicate two more cuts this year and another in 2026. According to the Federal Reserve’s latest “Beige Book” survey, economic activity is largely stable but revealed early signs of softening in consumer demand and hiring.

Inflation remains a growing concern. According to new analyses, consumers are now bearing the brunt of Trump’s sweeping import taxes. S&P Global estimates that U.S. companies have paid $1.2 trillion in tariffs so far this year, with nearly half ($592 billion) passed on to households through higher prices. The CPI is expected to have risen 3.1% in September, the highest since May 2024.

Weekly Earnings Roundup: Surprises & Misses

Several major companies released their earnings in the last 2 weeks, including Constellation Brands (NYSE: STZ), PepsiCo (NASDAQ: PEP), Delta Air Lines (NYSE: DAL), and Levi Strauss (NYSE: LEVI), JPMorgan Chase (NYSE: JPM), Johnson & Johnson (NYSE: JNJ), Wells Fargo (NYSE: WFC), Goldman Sachs (NYSE: GS), BlackRock (NYSE: BLK), Domino’s Pizza (NYSE: DPZ), Albertsons (NYSE: ACI), ASML Holding (NASDAQ: ASML), Bank of America (NYSE: BAC), Morgan Stanley (NYSE: MS), Abbott Laboratories (NYSE: ABT), Taiwan Semiconductor (NYSE: TSM), Interactive Brokers (NASDAQ: IBKR), and American Express (NYSE: AXP).

Constellation Brands: Reported Q2’26 EPS of $3.63 vs. $3.38 expected and revenue of $2.48 billion, slightly above forecasts. Management reaffirmed guidance for a 4%–6% drop in organic sales this year, citing weaker Hispanic demand tied to immigration and job concerns.

PepsiCo: Posted EPS of $2.29 vs. $2.26 expected and revenue of $23.94 billion. Strong international growth offset North American softness. Shares rose about 10% as the company reaffirmed stable full-year guidance for flat earnings and low single-digit revenue growth.

Johnson & Johnson: Q3 EPS of $2.80 beat estimates, with revenue up 6.8% to $23.99 billion. J&J will spin off its orthopedics unit within two years. Management expects growth through new drugs and expanded medical devices. Shares are up 10% since the earnings call.

American Express: Surpassed expectations with EPS of $4.14 versus $4.00 forecast, driven by 11% revenue growth to $18.43 billion. The company’s billed business reached $421 billion, ahead of estimates. Amex also unveiled an upgraded Platinum Card with new dining perks and a higher annual fee of $895. Shares rose after management signaled confidence in continued premium customer spending.

TSMC: Posted record Q3 profit, up 39% YoY, driven by AI-chip demand. Revenue hit NT$989.9 billion ($33.1 billion), exceeding estimates. Net income of NT$452.3 billion also topped forecasts, underscoring robust high-performance computing demand.

ASML: Reported €7.52 billion in Q3 sales, slightly below expectations, but profit of €2.13 billion edged higher. Management guided Q4 sales between €9.2-€9.8 billion with margins up to 53%. CEO warned of weaker 2026 China sales amid export curbs.

Top Gainers

Advanced Micro Devices (NASDAQ: AMD) shares jumped nearly 40% after OpenAI agreed to buy 6 gigawatts of AMD chips and received warrants for up to 10% of AMD shares if deployment milestones are met, cementing AMD’s role in AI hardware.

Trilog Metals (AMEX: TMQ) gained nearly 200% after the U.S. government announced a $36.5 million investment in the Alaska-based miner, securing a 10% ownership stake. The move marks Washington’s growing push to secure domestic access to critical minerals.

Bunge Global (NYSE: BG) climbed 21% last week after BMO Capital raised its price target. The stock benefited from renewed trade tensions as investors bet on higher demand for U.S.-sourced cooking oil following Trump’s threats to restrict Chinese imports.

Top Losers

Jefferies Financial (NYSE: JEF) shares dropped 18% after fallout from First Brands’ bankruptcy left lenders assessing their exposure. Jefferies disclosed that its Point Bonita Capital funds are owed about $715 million. The stock rebounded slightly later in the week as fears of systemic losses eased.

Klarna (NYSE: KLAR) Shares declined about 10%, slipping to $35 from its recent IPO price of $40. The pullback reflects investor skepticism toward the buy-now-pay-later sector amid tighter regulation, elevated funding costs, and concerns about credit risk.

Upcoming Earnings: Key Stocks to Monitor

Current week’s spotlight will turn to several major names, including Netflix (NASDAQ: NFLX), General Electric (NYSE: GE), Coca-Cola (NYSE: KO), Texas Instruments (NASDAQ: TXN), Lockheed Martin (NYSE: LMT), Tesla (NASDAQ: TSLA), SAP (NYSE: SAP), IBM (NYSE: IBM), T-Mobile (NASDAQ: TMUS), Intel (NASDAQ: INTC), and Procter & Gamble (NYSE: PG).

The following week will feature tech and industrial heavyweights such as Visa (NYSE: V), UnitedHealth (NYSE: UNH), Booking Holdings (NASDAQ: BKNG), Microsoft (NASDAQ: MSFT), Alphabet (NASDAQ: GOOGL), Meta Platforms (NASDAQ: META), ServiceNow (NYSE: NOW), Verizon (NYSE: VZ), Boeing (NYSE: BA), Apple (NASDAQ: AAPL), and Eli Lilly (NYSE: LLY).

With AI-driven optimism, trade frictions, and central bank policy still in flux, the upcoming earnings cycle will be critical for gauging whether corporate fundamentals can sustain market momentum, or whether macro headwinds will finally start to weigh on sentiment.