The S&P 500 started November on unstable footing, reflecting a market caught between optimism over easing inflation pressures and anxiety over an intensifying AI spending controversy. From October 31 to November 7, the index fell 1.63%. The following week offered only a faint recovery. Overall, the two-week period closed with a 1.55% decline.

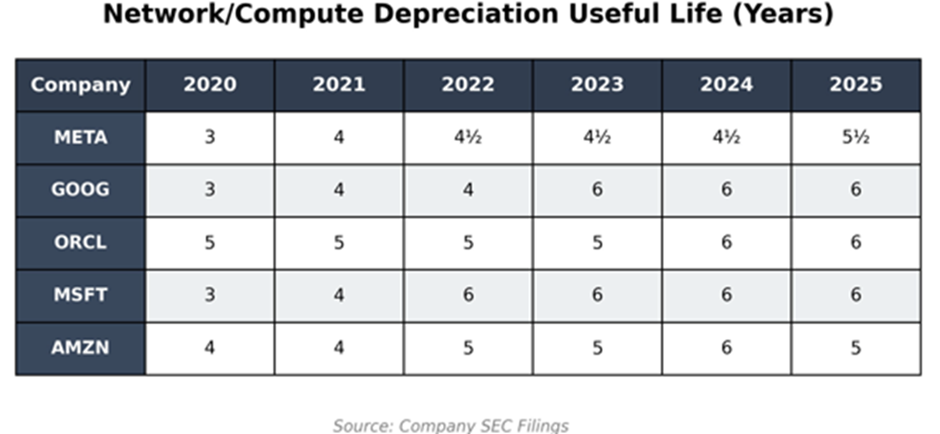

A new source of tension came from an unexpected voice. Michael Burry warned that large technology companies are materially understating depreciation tied to AI data centers. “By my estimates they will understate depreciation by $176 billion 2026-2028. By 2028, ORCL will overstate earnings 26.9%, META by 20.8%, etc. But it gets worse,” he wrote. The comment reverberated across the market, with investors suddenly questioning whether the AI boom is masking a quieter imbalance in corporate accounting.

Just days later, that concern spilled into the public arena when a tense confrontation unfolded between Sam Altman and investor Brad Gerstner during a podcast interview. Gerstner pressed Altman on how OpenAI could justify $1.4 trillion in long-term spending commitments on compute and infrastructure while generating roughly $13 billion in annual revenue. Altman bristled at the implication, snapping, “If you want to sell your shares, I’ll find you a buyer.” The exchange went viral, feeding a narrative that even AI’s most influential leaders are feeling the pressure to defend their financial bets.

These two events have increasingly been cited as catalysts for the market’s recent pullback, dragging sentiment lower at a moment already clouded by political uncertainty. The Trump administration is reportedly preparing to reduce tariffs on imports such as coffee, bananas, beef and other food products from Argentina, Ecuador, Guatemala and El Salvador to alleviate price pressures. Meanwhile, the historic 43-day federal shutdown that left 1.25 million workers furloughed or unpaid has officially ended. Still, policymakers estimate roughly $11 billion in economic activity was permanently lost, while delayed data releases and travel disruptions will weigh on visibility for weeks ahead.

Investors are now watching the market closely as it approaches a critical support level. If this floor breaks, traders worry that the selling could accelerate. The IMF’s recent assessment reinforced those concerns by flagging slower job growth, weakening domestic demand, trade friction and the lasting drag of the 43-day shutdown on Q4 output.

Bitcoin added to the unease, sliding to $94,500, its lowest point since May and a sharp reversal from the overnight high above $100,000. In equities, policy and industry news continued to reshape expectations. Microsoft and Amazon are supporting legislation that would further restrict Nvidia’s ability to sell advanced chips to China, a move that could reshape the global semiconductor supply chain. Meanwhile, Paramount, Comcast and Netflix are preparing bids for Warner Bros. Discovery, setting up what could become one of the biggest media consolidation battles in years.

Weekly Earnings Roundup: Surprises & Misses

Several major companies released their earnings in the last 2 weeks, including Palantir (NASDAQ: PLTR), Ryanair (NASDAQ: RYAAY), AMD (NASDAQ: AMD), Uber (NYSE: UBER), Spotify (NYSE: SPOT), Pfizer (NYSE: PFE), Novo Nordisk (NYSE: NVO), McDonald’s (NYSE: MCD), AppLovin (NASDAQ: APP), Robinhood (NASDAQ: HOOD), AstraZeneca (NASDAQ: AZN), and Airbnb (NASDAQ: ABNB).

Palantir: Quarterly results exceeded expectations once again. Q3 revenue jumped 63% year over year to $1.18 billion, marking its second straight quarter above the billion-dollar threshold. Net income surged to $475.6 million from $143.5 million a year ago. But despite the strong fundamentals, shares slid 10% over the past two weeks as valuation concerns intensified. News that Michael Burry’s Scion Asset Management has taken short positions against Nvidia and Palantir further amplified those fears, pushing investors to reassess whether the stock’s lofty premium is sustainable.

AMD: Q3 profit rose to $1.96 billion, or $1.20 per share, compared with $1.5 billion a year earlier. Sales strengthened across both AI accelerators and PC processors, reflecting market gains even as broader semiconductor sentiment wavered.

Disney: Reported mixed results, sending shares down 7.8%. Revenue of $22.46 billion came in slightly below expectations and flat year over year. Strong performance in theme parks and streaming could not offset ongoing declines in linear television.

CoreWeave: Shares tumbled nearly 40% in the past two weeks after the company cut its full-year revenue outlook. The delay in fulfilling a major customer contract reduced 2025 revenue expectations to a range of $5.05 billion to $5.15 billion. Quarterly revenue still beat estimates at $1.36 billion, and losses were narrower than expected, but growth doubts overshadowed the beat.

AppLovin: Delivered another strong quarter with revenue up 68% to $1.41 billion and adjusted earnings of $2.45 per share. Yet the stock fell 15% this week after news broke that the SEC is investigating the company’s data-collection practices.

Robinhood: Posted a standout quarter, with net income up 271% to $556 million, or $0.61 per share, beating expectations. Crypto-trading revenue rose sharply but still fell short of analyst forecasts. The company announced new initiatives to diversify its revenue streams, including a mortgage partnership with Sage Home Loans and a closed-end fund to give retail investors access to private markets.

Top Gainers

Eli Lilly (NYSE: LLY) share price surged by 13% over the two weeks. Strong demand for its GLP-1 therapies and expectations around expanded U.S. government access fueled the rally. The company beat earnings expectations and raised its full-year outlook, edging closer to becoming the first pharmaceutical firm to surpass a $1 trillion valuation. Analysts highlighted the recent pricing agreement with Washington, which could broaden eligibility for Medicare and Medicaid patients in 2026.

Dollar General (NYSE: DG) rose 5% over the past week as analysts continued to boost price targets. UBS set a $135 target, while Barclays issued a $127 target, citing improved operational execution and early signs of a turnaround strategy taking hold.

Top Losers

SMCI (NASDAQ: SMCI) plunged 30% in the past two weeks after reporting weaker-than-expected fiscal Q1 results. Revenue fell 15% year over year to $5.94 billion, far below earlier guidance of $6 billion to $7 billion. Net income declined to $168.3 million, marking a sharp contraction from last year’s AI-driven highs.

MicroStrategy (NASDAQ: MSTR) fell roughly 25% as Bitcoin weakened. Social media rumours suggested the company may have sold into the crypto slide.

Oracle (NYSE: ORCL) declined 15%, extending a multi-week slide that has erased more than $250 billion in market value since September. Concerns center on the company’s aggressive AI buildout, heavy debt financing, and the sheer scale of its infrastructure expansion. Oracle now carries $96 billion in long-term debt, up sharply from $75 billion last year, and analyst forecasts suggest this could rise to nearly $300 billion by 2028.

Upcoming Earnings: Key Stocks to Monitor

Next week’s spotlight will shift to Trip.com (NASDAQ: TCOM), Home Depot (NYSE: HD), Pinduoduo (NASDAQ: PDD), Nvidia (NASDAQ: NVDA), and Walmart (NYSE: WMT).

The following week will feature Alibaba (NYSE: BABA), Dell (NYSE: DELL), and HP (NYSE: HPQ).

With macro uncertainty building and concerns of an AI bubble intensifying, the upcoming earnings cycle will be crucial in determining whether markets enter a sustained boom or risk a sharp correction.