The S&P 500 moved in different directions over the past two weeks as markets struggled to find conviction. Overall, the index declined by 0.31% as investors digested a series of macro and policy developments.

The week began with the Federal Reserve’s 09 December meeting, which set the early tone. Policymakers lowered the benchmark rate to a range of 3.50% to 3.75%, the lowest level in nearly three years. Chair Jerome Powell struck a cautious note, stressing that further cuts are not guaranteed and will depend on incoming data. Despite that message, markets are increasingly pricing in additional easing in 2026 as growth momentum cools.

Markets also watched commodities and crypto closely. Gold prices hovered near multi-week highs around $4,280 per ounce as investors positioned for eventual rate cuts and sought protection against volatility. Bitcoin experienced sharp swings but recently stabilized near $92,000, recovering modestly as risk appetite improved toward the end of the week.

The real shift in sentiment came on Friday. Negative AI sentiment proved to be the game changer, pushing the S&P 500 down 1.1% and sending the Nasdaq lower by 1.7%. Stocks most exposed to AI infrastructure were hit hardest. Nvidia declined as much as 3.2%, CoreWeave dropped 11%, Oracle slid 4% and Broadcom fell 11%. The pullback reflects growing unease that hyperscaler spending on data centers may be approaching a more mature phase after an aggressive buildout cycle. High-profile investors such as Michael Burry have drawn comparisons to the dot-com era bubble of the late 1990s, raising concerns among investors about how the broader market could react if enthusiasm around AI fades after driving much of the S&P 500’s 17% gain year to date.

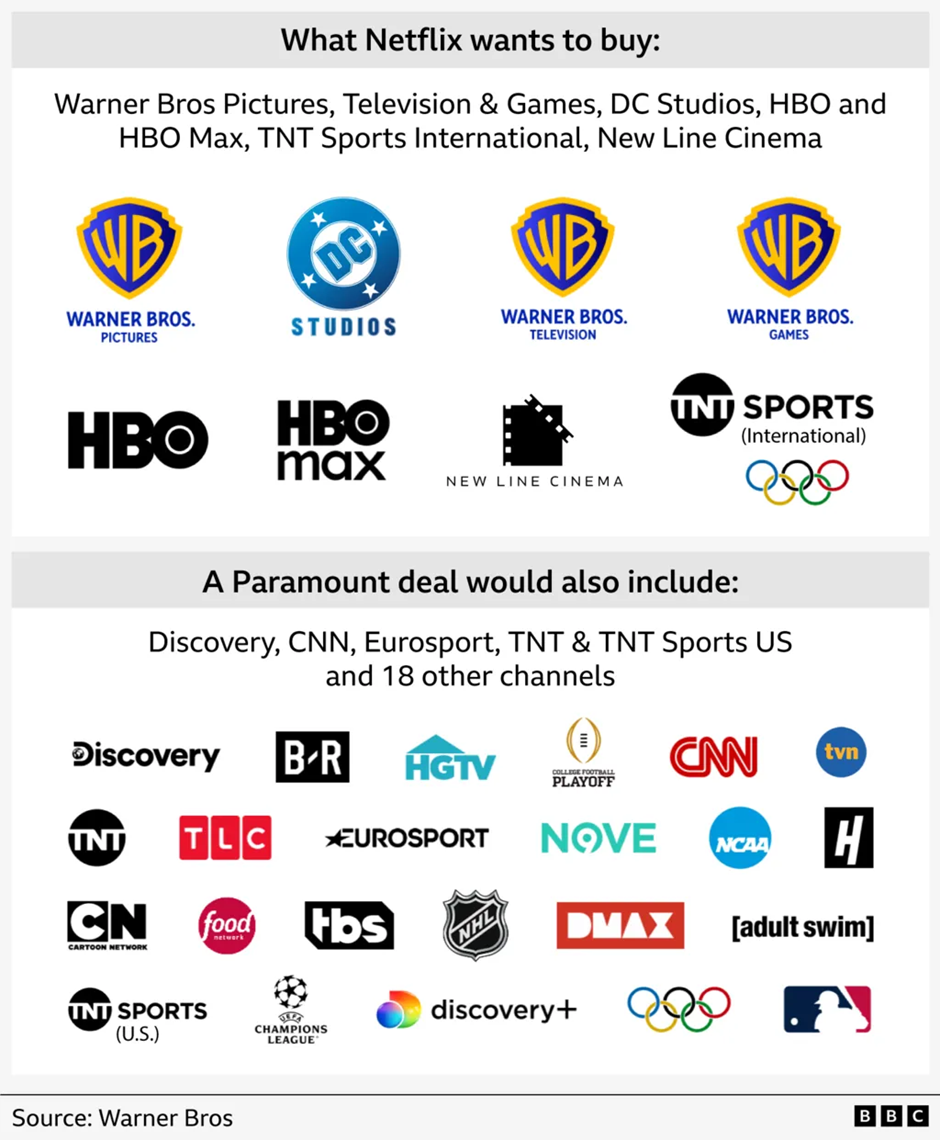

Meanwhile, the proposed acquisition of Warner Bros Discovery continues to dominate headlines as Netflix and Paramount Skydance are involved in a high-stakes bidding war. David Ellison of Paramount Skydance took a $108.4 billion offer directly to investors after Warner Bros’ board approved a competing $82.7 billion bid from Netflix. Warner Bros. brings a century-old content library, including iconic franchises such as Looney Tunes, Friends, Superman, and Harry Potter. Netflix’s proposal is for Warner Bros. Studios and streaming networks to spin off the rest of the company as a standalone entity. Paramount, in contrast, is seeking complete control of Warner Bros, including its traditional pay TV networks, which are seen as a declining business. While consolidation could reshape streaming, it has also raised serious regulatory and antitrust concerns.

In technology, Elon Musk confirmed that SpaceX is targeting a public listing in 2026, following a recent share sale valuing the company at $800 billion. The future of data infrastructure also took an unexpected turn after Nvidia-backed startup Starcloud trained an AI model in space for the first time, hinting at the possibility of space data centers as energy constraints grow on Earth.

Established players continued to benefit from the AI cycle. Cisco closed at a record high for the first time since 2000, lifting its market value to $317 billion, as CEO Chuck Robbins highlighted $1.3 billion in quarterly AI infrastructure orders from major web companies. Lululemon also drew attention after announcing a CEO change, as the pricey yoga-wear brand looks to reignite growth amid pressure from upstart competition and its founder. The share price jumped nearly 10% post-announcement.

Confluent shares were also in focus, surging 29% after IBM announced an $11 billion acquisition of the company. The deal is aimed at strengthening IBM’s AI and data capabilities as global data volumes surge.

Weekly Earnings Roundup: Surprises & Misses

Several major companies released their earnings in the last 2 weeks, including Credo Technology (NASDAQ: CRDO), MongoDB (NASDAQ: MDB), Salesforce (NYSE: CRM), Snowflake (NYSE: SNOW), Toronto-Dominion Bank (NYSE: TD), Adobe (NASDAQ: ADBE), Synopsys (NASDAQ: SNPS), Broadcom (NASDAQ: AVGO), and Costco (NASDAQ: COST).

MongoDB stood out with a strong quarter, beating Wall Street expectations and issuing a strong outlook. Revenue surged 19% YoY to $628 million, exceeding forecasts. Adjusted earnings came in at $1.32 per share, well above estimates. The stock has climbed 28% over the past two weeks.

Credo Technology reported explosive growth, with revenue jumping more than 270% YoY to $268 million and adjusted earnings per share beating consensus by 37%. Despite strong fundamentals, the stock is down 16% over the past two weeks amid broader concerns about AI infrastructure spending.

Salesforce posted solid fiscal third-quarter results, with revenue rising 8.6% to $10.3 billion and adjusted earnings of $3.25 per share. The company continued to deepen its AI strategy through acquisitions and product launches, including its Agentforce platform. Management also issued a bold $60 billion ($35 billion revenue in FY24) revenue target for fiscal 2030, exceeding analyst expectations. Share price is up 12% over the past two weeks.

Broadcom reported strong results with total revenue up 28% and AI chip sales rising 74%. Net income climbed 97% to $8.51 billion. Despite the performance, shares are down 7% over the past two weeks amid broader concerns about AI valuations.

Oracle disappointed the market after reporting revenue of $16.1 billion (up 14% YoY) and announcing delays to key data centers supporting OpenAI workloads. The company also warned that capital expenditures for fiscal 2026 will be significantly higher than previously expected. Shares fell sharply, dropping 11% in a single session on Thursday and ending the two-week period down 5%.

Top Gainers

Warner Bros Discovery (NASDAQ: WBD) surged 25% amid an intensifying bidding war between Netflix and Paramount Skydance.

Dollar General (NYSE: DG) jumped 22% after beating earnings expectations and lifting its profit forecast. Slowing labour momentum and rising economic uncertainty are pushing consumers to become more value-conscious, seeking cheaper alternatives and better seasonal deals. The shift is lifting discount retailers across the board, with Dollar Tree (NASDAQ: DLTR) also climbing 18% over the past two weeks.

Western Digital (NASDAQ: WDC) rose 7% over the past two weeks and is up roughly 216% over six months, supported by sustained demand for high-capacity storage tied to AI infrastructure. The company is also set to join the Nasdaq 100.

Top Losers

Netflix (NASDAQ: NFLX) fell 13% over the past two weeks as investors weighed regulatory risks and financial uncertainty surrounding its pursuit of Warner Bros Discovery.

Marvell Technology (NASDAQ: MRVL) dropped 8% after an analyst downgrade raised concerns about losing key AI chip design contracts.

High Revenue Growth Leaders

For investors tracking revenue momentum, Streamlined Finance’s Earnings Indices page provides a comprehensive view of companies delivering strong growth this earnings season. Standout companies include Coinbase, which posted 47% YoY revenue growth; Robinhood, up 75%; NVIDIA, reporting 65%; and AppLovin, with 55% growth.

Upcoming Earnings: Key Stocks to Monitor

The next week will bring earnings from Micron Technology (NASDAQ: MU), Jabil (NYSE: JBL), General Mills (NYSE: GIS), Accenture (NYSE: ACN), Nike (NYSE: NKE), FedEx (NYSE: FDX), and Carnival (NYSE: CCL). The coming week is relatively quiet, with no major companies scheduled to report earnings.

AI sentiment is likely to remain a key driver for markets as investors navigate the holiday period and begin looking toward 2026.